Mayo Pension Payment Options

Updated May 2026

The views in this blog are the views of Fortress Financial and not the views of Mayo Clinic. Mayo Clinic and Fortress Financial Group are not affiliated.

Quick answer: Mayo Clinic’s pension lets you choose among eight payment forms: a life-only annuity; life-only with a 5, 10, or 15-year term certain; 50%, 75%, or 100% joint and survivor annuities; a 66.7% or 100% joint and survivor with a 5-year term certain; or a single lump sum. Anything other than life only reduces your monthly payment. The right choice depends on marital status, survivor needs, longevity expectations, and how the pension fits with your other retirement income.

Below, we walk through every option Mayo offers, how each one trades monthly income for survivor protection, what the defaults are if you don’t actively elect, and the practical questions we help Mayo retirees work through before they sign their election forms.

How does the Mayo pension actually work in 2026?

Mayo’s pension is a defined benefit plan covered by federal ERISA rules and insured by the Pension Benefit Guaranty Corporation. Per the January 2026 Summary Plan Description, your benefit is calculated under one of three formulas depending on when you became eligible and what you elected during the 2023 Mayo Retirement Choice window: Final Average Pay (service through December 31, 2014), Annual Accumulation (January 1, 2015 forward), or Stable Lump Sum (January 1, 2023 forward, or if you elected to switch during the August 14 to September 15, 2023 Choice window). All three formulas cap benefit service at 30 years.

Whichever formula calculated your benefit, you still have to decide how to receive it: as a stream of monthly payments, as a single lump sum, or as one of the joint and survivor variations Mayo offers. That election is what this article is about.

In our planning conversations with Mayo retirees, we find this is often the single biggest decision people make at retirement, and it’s the one most people want to talk through more than once.

What are the monthly payment options Mayo offers?

Mayo offers eight forms of payment, plus the lump sum. Anything other than life only reduces the monthly amount, because Mayo is insuring more than just your life.

Life only annuity

Monthly payments for your lifetime. Payments stop the day you die, with nothing continuing to anyone else. This produces the highest monthly check of any option because Mayo only insures one life. If you’re unmarried and don’t actively elect another form, this is your default.

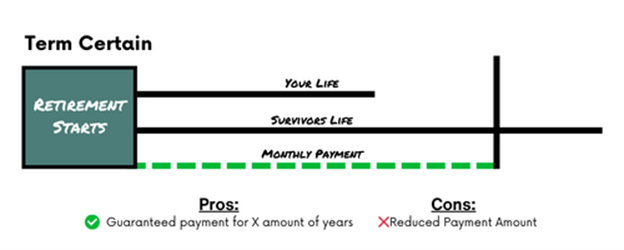

Life only with a 5, 10, or 15-year term certain

Same monthly amount during your life, with a guarantee that payments continue to a named beneficiary for the balance of the term if you die early. Example: you elect a 15-year term certain and die five years in. Your beneficiary receives ten more years of payments at your monthly amount, then payments stop. Choosing 15 years reduces the monthly payment more than 5 years, because the guarantee is longer.

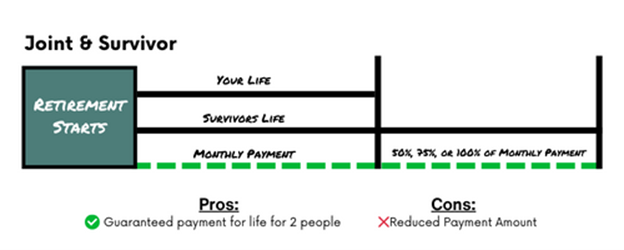

50%, 75%, or 100% joint and survivor annuity

Monthly payments to you for life, and if your joint annuitant (typically your spouse) outlives you, payments continue to them for their life at the percentage you elected. If your joint annuitant dies before you, your monthly payment doesn’t change. The higher the survivor percentage, the more Mayo will pay over time, so the lower your monthly amount.

Example: you elect 50% joint and survivor and die ten years in. Your spouse receives half of your monthly amount for the rest of their life.

66.7% or 100% joint and survivor with a 5-year term certain

A blend. Your full pension runs for five years guaranteed. After the five-year term, if you die, your joint annuitant receives 66.7% or 100% of your monthly payment for their lifetime. If both you and your joint annuitant die within the first five years, a designated beneficiary receives the remaining payments to complete the five-year term.

Lump sum

The present value of your benefit, paid in one payment. Mayo calculates the lump sum using IRS-prescribed interest rates and mortality assumptions in effect at your benefit commencement date, so the same person retiring six months later may see a different amount. If you don’t roll the lump sum directly to an IRA or another qualified plan, 20% of the value is automatically withheld for federal income tax. Lump sum is also the automatic form if the present value of your benefit is $1,000 or less, regardless of what you elect.

Which option is the default if I don’t choose?

If you’re married at your benefit commencement date and don’t make an active election, Mayo defaults you to a 50% joint and survivor annuity. If you’re unmarried, the default is the life-only annuity. If you’re married and want to elect anything other than a 50%, 75%, or 100% joint and survivor with your spouse as the joint annuitant, your spouse must consent in writing in front of a notary public, within 90 days of the first day of the month payments begin.

One rule that surprises people: once monthly payments start, your joint annuitant designation is irrevocable. You can’t change it after the annuity start date, even if your spouse predeceases you or you later divorce. If you elect 50% joint and survivor with your spouse and your spouse dies five years later, the benefit doesn’t redirect, and your monthly payment doesn’t go up. (Beneficiaries on a term certain piece of the benefit can still be updated.)

How do the options compare side by side?

The table below summarizes the tradeoffs. The exact dollar reduction for each option depends on your age, your joint annuitant’s age, and the IRS interest rates in effect at your commencement date, so request a personalized estimate from Mayo HR before you elect.

| Option | Who it fits | Survivor benefit | Tradeoff vs life only |

|---|---|---|---|

| Life only | Single retirees, or married couples whose spouse has independent income | None. Payments stop at your death. | Highest monthly payment of any option. |

| Life only with 5, 10, or 15-year term certain | Retirees who want some downside protection without naming a joint annuitant | Beneficiary receives the balance of the term if you die early. | Modest reduction; longer term means lower monthly amount. |

| 50%, 75%, or 100% joint and survivor | Married retirees whose spouse needs ongoing income | Joint annuitant receives 50%, 75%, or 100% of your payment for their lifetime. | Reduction grows with the survivor percentage and the age gap. |

| 66.7% or 100% joint and survivor with 5-year term certain | Couples wanting both survivor income and a short guaranteed period | Joint annuitant receives 66.7% or 100% for life; beneficiary gets remainder of 5 years if both die early. | Larger reduction than a plain joint and survivor at the same percentage. |

| Lump sum | Retirees who want flexibility, control, or to consolidate with other retirement assets | Whatever remains in the account passes to your beneficiaries. | Replaces lifetime income with a one-time payment; subject to investment, withdrawal, and tax decisions. |

How should I think about choosing among these options?

We walk Mayo retirees through four questions before they sign:

1. Who else relies on this income? If you’re single with no dependents, life only and lump sum are the cleanest. If you’re married, the question becomes how much income your spouse needs if you die first, and whether other resources (your spouse’s Social Security, your 403(b), your taxable savings) can cover the gap.

2. What’s your honest read on longevity? Annuity options reward long life. If you have a strong family longevity history and you’re in good health, monthly options may provide more total lifetime payments, depending on lifespan, rates, and investment outcomes. If your health is uncertain and you have other income, a lump sum or short term certain may serve your family better.

3. Do you want flexibility, or a guaranteed paycheck? A lump sum gives you control. You decide how to invest, when to withdraw, and what to leave behind. The tradeoff is sequence-of-returns risk, withdrawal-rate discipline, and the responsibility to manage the money yourself, often for thirty years. The annuity gives you a paycheck for life, no investment decisions required.

4. What’s the tax picture? A lump sum rolled to an IRA is not a taxable event. If you take the cash, the entire amount is ordinary income in the year received, with 20% mandatory federal withholding. Monthly payments are taxed as you receive them, smoothing the income across years and bracket lines.

For a closer look at the broader tradeoff between a single payment and a lifetime stream, see our piece on lump sum versus monthly income from a Mayo pension.

How does this fit with the rest of your Mayo retirement?

Your pension is one piece of a Mayo retirement, alongside your 403(b), Social Security, retiree healthcare, and any taxable savings. The pension election shouldn’t be made in isolation. The same household with the same pension might rationally choose a lump sum if the spouse has substantial other income, and a 100% joint and survivor if the spouse doesn’t.

If you’re still earlier in the planning process, our 2026 Mayo Clinic pension guide walks through how the benefit accrues, and our Mayo 403(b) guide covers the other big piece of your Mayo retirement income. Both are worth reading before you sit down to elect a payment option. The Mayo retirement FAQ collects the questions we hear most often from people in their final twelve months at Mayo. For a fuller picture of how the pension fits alongside your other Mayo benefits, our overview on building wealth as a Mayo Clinic employee is a useful companion read.

What does this look like for Rochester and Scottsdale retirees?

Most of the Mayo retirees we work with live in Rochester and the surrounding southeast Minnesota area, where Minnesota state income tax applies to pension and IRA income (subject to the Social Security and pension subtractions). Some plan to spend retirement in Scottsdale or another lower-tax state. The payment form you elect doesn’t change your tax residency, but it does change how much taxable income hits in which year. A lump sum rolled to an IRA defers the tax. A lump sum taken in cash creates a single large taxable event, which can push you into a higher Minnesota bracket and trigger Medicare IRMAA surcharges two years later. Monthly payments smooth the tax impact, but commit you to the income pattern of your state of residency in retirement. We talk through this carefully with clients planning a snowbird arrangement. Keep in mind that state tax rules vary. For a deeper look at how the pension supports a stable monthly cash flow, see how to turn your retirement savings into a reliable monthly paycheck, and on the claiming side, when should I take Social Security.

What this means for you

The right Mayo pension election is the one that fits your household, your other income, and your view of risk. There’s no single answer that’s right for everyone, and the form you elect is, with limited exceptions, locked in once payments begin. If you’re within twelve months of retirement, this may be an appropriate time to model the options against your full income picture, not just your monthly budget.

Frequently asked questions

When does my Mayo pension actually start paying?

Your benefit commencement date is the first day of a future month after you terminate employment. Monthly annuity payments arrive on the last business day of the month, beginning with the month of your commencement date. If you’re already retirement-eligible and give Mayo at least 30 days’ notice, you’ll receive your distribution application about four to six weeks before your target start date.

Can I take my Mayo pension as a lump sum and roll it to an IRA?

Yes. Mayo allows lump sum as an optional form of payment for any of the three benefit formulas. If you roll the lump sum directly to an IRA or another qualified plan, no federal tax is withheld at distribution. If you take it as cash, 20% is automatically withheld for federal income tax, and the entire amount is taxable in the year you receive it.

What happens to my Mayo pension if I die before payments begin?

If your benefit is vested and you die before your commencement date, Mayo provides an automatic death benefit equal to what your joint annuitant would have received under a 50% joint and survivor annuity, calculated as if you had started payments the day before you died. Your beneficiary can elect to receive that amount as a life annuity or a lump sum.

Why does my monthly amount drop so much for a 100% joint and survivor election?

Because Mayo is now insuring two lives instead of one, and at 100% the surviving spouse’s payment is the same as yours. The actuarial cost of guaranteeing the higher survivor benefit shows up as a lower monthly check during your lifetime. The reduction depends on your age and your joint annuitant’s age at your benefit commencement date.

I picked my joint annuitant. Can I change them later?

Generally no. Once your annuity start date passes, your joint annuitant designation is irrevocable, even if your spouse predeceases you or you later divorce. You can update beneficiaries on any term certain portion of your benefit, but you cannot redirect the survivor annuity to a new person.

How does the Stable Lump Sum formula change my payment options?

Even if your benefit was calculated under the Stable Lump Sum formula (which applies to anyone hired or rehired into eligibility on or after January 1, 2023, or who elected to switch during the 2023 Mayo Retirement Choice window), you still get the full menu of payment forms. Mayo converts the lump sum value to a monthly annuity at commencement using IRS-prescribed interest rates and mortality, and you elect from any of the standard options.

Disclosures

This article is for educational purposes only and does not constitute personalized investment, tax, legal, or financial advice. The information provided is general in nature and may not apply to your specific situation. Please consult with a qualified financial advisor, tax professional, or attorney about your individual circumstances before making any financial decisions.

Fortress Financial Group is a Registered Investment Adviser. Registration does not imply a certain level of skill or training. Fortress Financial Group operates as a fee-only fiduciary.

This article describes Mayo Clinic retirement benefits as we understand them based on publicly available information and our experience working with Mayo Clinic employees and retirees. Plan provisions can change, and your specific benefits depend on your hire date, employment classification, and other factors. Consult Mayo Clinic Human Resources, your plan documents, or a qualified advisor for guidance specific to your situation. The views in this blog are the views of Fortress Financial and not the views of Mayo Clinic. Mayo Clinic and Fortress Financial Group are not affiliated.

Tax laws and regulations change frequently. The information in this article reflects rules in effect as of May 2026 and may not reflect subsequent changes. Tax outcomes depend on your specific situation. Consult a qualified tax professional before making decisions based on tax considerations.

Past performance is not indicative of future results. All investments involve risk, including potential loss of principal. References to specific strategies or asset classes are illustrative and are not recommendations to buy or sell any security. Diversification does not guarantee a profit or protect against loss in declining markets.

Statements about future market behavior, economic conditions, longevity, or planning outcomes are forward-looking and subject to numerous risks and uncertainties. Actual results may differ materially. Use forward-looking statements as one input among many, not as a basis for specific decisions.

Free Download

The Seven Most FAQs About Retiring From Mayo

The views in this page are the views of Fortress Financial and not the views of Mayo Clinic.

Mayo Clinic and Fortress Financial Group are not affiliated