Mayo Pension Payment Options

The views in this page are the views of Fortress Financial and not the views of Mayo Clinic.

Mayo Clinic and Fortress Financial Group are not affiliated

Choosing the monthly payment route for your Mayo Pension is a significant decision. However, it's not the only one. You also need to consider your survivor benefits, a choice that carries its own weight and importance.

Mayo offers several different options for monthly payments: life only, term certain, and a percentage for joint and survivor annuities. It is important to note that anything outside the Life Only option will reduce monthly payments. For details, please consult Mayo Clinic Human Resources.

Life Only: This option is as straightforward as it gets. You'll receive monthly payments for your life; once you're gone, the payments stop. If you're single, this is the default option Mayo provides.

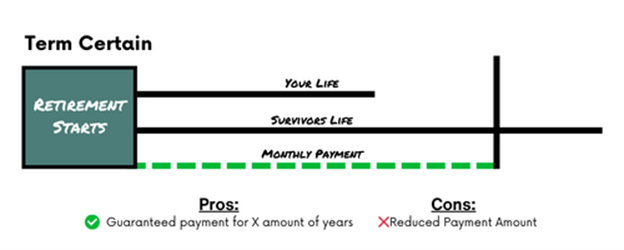

Term Certain: This option is similar to life only, but it guarantees that payment will continue to your beneficiary for a certain number of years after you pass away. For example, if you selected a 15-year term certain and passed away five years into retirement, your beneficiary will receive ten more years of pension payments. Mayo Clinic allows you to select 5, 10, or 15 years for certain terms.

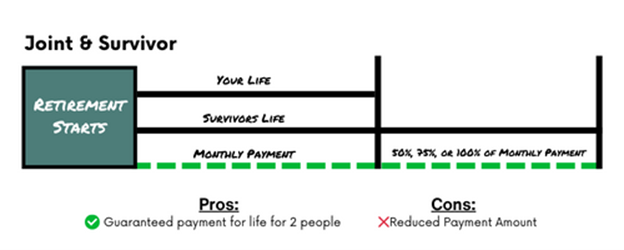

Joint & Survivor Annuity: Under this option, you will receive your monthly payment, and if you pre-decease your joint annuitant (typically your spouse), they will receive your monthly payment for the remainder of their life. You select if they receive 50%, 75%, or 100% of your monthly payment. For example, if you select 50% joint and survivor annuity and pass away ten years into retirement. Your joint annuitant will receive 50% of your monthly payment for the remainder of their life.

Joint & Survivor with Term Certain: This blends the two previous options. Your full pension is guaranteed for five years, with an option for your joint annuitants to receive 66.7% or 100% of your pension if you pre-decease them. The added benefit is this: If you and your joint annuitant pass away within the five-year period, a designated beneficiary will receive payments for the remaining term. Here is an example: You retire and select joint & survivor with the term certain; you and your spouse pass away two years into retirement. A designated beneficiary will receive your monthly payment for the next three years.

Conclusion: Deciding which option is right for you is a personalized decision. Having support from an advisor who has worked with people in your shoes can help alleviate some of the angst that comes with making this and other retirement decisions.

Disclosure:

Fortress Financial Group, LLC (“Fortress”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Fortress and its representatives are properly licensed or exempt from licensure. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fortress and its advisors do not provide accounting or tax advice. Consult your tax professional.

Free Download

The Seven Most FAQs About Retiring From Mayo

The views in this page are the views of Fortress Financial and not the views of Mayo Clinic.

Mayo Clinic and Fortress Financial Group are not affiliated